We the People put together a system here with schools, universities, scientific research, courts, a stable financial/monetary system, infrastructure like roads, dams, airports, and all the other components of a (used-to-be) prospering economy. That takes money, and naturally we expect the beneficiaries of all of that investment to give back into the system. But then the beneficiaries of that system figure out ways to get around paying back – and the larger and wealthier they are the more ways they find to give back even less.

Jeeze, look at what we learned about Apple!

It is time for Americans to change to a tax system that really gets corporations to pay their fair share – and stop letting them move their taxable income all over the world.

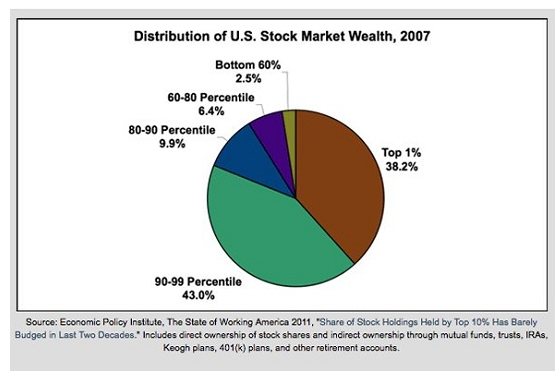

Who Pays Corporate Taxes

Any discussion of corporate taxes should begin with an understanding of what (who, actually) we are talking about. This chart shows who owns the corporations:

As of 2007 the top 1 percent owned 38.2 percent of corporate stock. The next 9 percent owned an additional 43 percent. For the math-challenged, that means the top 10 percent owned 81.2 percent of all corporate stock. The bottom 60 percent of us owned 2.5 percent.

When we talk about taxing corporations, we are really talking about taxing the wealthiest few.

The Current Problem

The top corporate tax rate used to be higher (53%, then 46%), but multinational corporations complained that those rates made them "less competitive," so we "reformed" it down to 35 percent. Then these giant companies went from country to country, complaining that their tax rates made businesses "less competitive" and these countries "reformed" their tax rates. So now our rates again are higher than rates in many other countries. This "downward spiral" has shifted taxes worldwide away from the top few, and governments have fewer resources.

Big Mistakes In Current Corporate Tax Laws

U.S. companies that earn profits outside our borders \have to pay the corporate tax on their income minus any taxes they pay to other countries. So if a company makes $1,000 profit in Axylvanistan and pays them a tax rate of 10%, they only have to pay a tax rate of 25 percent here. But a mistake in current tax law lets companies "defer" paying these taxes until they "repatriate" the money, or "bring it home."

Caused Jobs, Factories, Profit Centers To Leave The Country

To take advantage of this loophole companies started moving jobs, factories and profit centers out of the country to keep their profits from being made inside the U.S. One scheme, for example, involves transferring intellectual property (patents, etc.) to a subsidiary registered in a tax-haven country and making it appear that a big part of your costs are intellectual property license fees paid to that subsidiary. (This is why you hear about "Double Irish" and "Dutch Sandwich" tax schemes and subsidiaries that are only mailboxes in tax-haven counties, etc.) Soon these giant multinationals were holding many billions of dollars outside of the country to "defer" their taxes.

Then these companies came to the government and offered to bring that big hoard of money back to the U.S. and use it to "create jobs" if we would just charge them a really low tax rate -- just this once. So we gave them a "repatriation tax holiday" in 2004. The companies brought the money back, and not only didn't "create jobs," they doubled down on the scheme, moving even more jobs, factories and profit centers out of the country. ("Hey, they fell for it, now we know how to avoid taxes forever!")

We Gave In, So They Did It More

Now after moving more jobs, factories and profit centers out of the country these multinational corporations are holding somewhere between $1.7 and $2 trillion in subsidiaries outside the country, untaxed. Apple alone has over $100 billion outside the country. Google reported $10 billion in profits in Bermuda in 2011. And these companies say they will not bring the money back without another "tax holiday."

This $1.7-2 trillion of untaxed represents up to $750 billion we could use for schools, BRIDGES, high-speed rail, infrastructure jobs, you name it -- all things we are really need to be doing now, to make all of our lives better. So this is serious business.

Possible Solutions

Senator Bernie Sanders (I-VT) and Representative Jan Schakowsky (D-IL) have introduced the Corporate Tax Fairness Act that just ends the deferral, so these companies have to just bring the money back, pay their taxes, and end all the schemes to take advantage of this loophole.

Friday's New York Times had a "Room for Debate" roundtable discussion, Getting a Fair Share From Multinationals, with differing points of view. The suggestions range from the multinational corporate idea: "Don't tax us at all" to a "minimum tax rate" that guarentees We the people a small slice of the pie, at least.

In this discussion Alan J. Auerbach of the University of California at Berkeley offers a good diea, Tax Earnings Where Products Are Sold. The idea is simple: tax these companies where they sell, not where they claim the profits are made.

The fundamental problem is our reliance on the concepts of residence, or where a company is located, and source, or where the company’s assets and production activities are located. These concepts may have worked reasonably well in the 1930s, but they do not hold up when confronting a multinational company with global operations.

... A better approach would be to tax a company’s earnings based on where its products are sold, using what is known as the destination approach. For example, earnings from the production of a smart phone sold in the United States would be subject to U.S. corporate tax, regardless of the company’s residence or where the company reports its production to have occurred.

Using destination to determine tax liability would allow the United States to impose tax on its fair share of multinational earnings while eliminating any incentive for companies to move their activities or themselves to other countries, since the same U.S. tax would still apply regardless of residence or source.

Roger Hickey wrote about this idea the other day, in his CAF post, Apple: Bad Model for “Tax Reform.” California, New Tax Thinkers, Chart a Better Way,

This new tax system would provide companies absolutely no tax incentive to move production to lower-tax countries. And with the costs of transportation and wages going up around the world, U.S. and non-U.S. companies would likely accelerate the trend toward manufacturing (and hiring) where they sell. And small businesses, now at a disadvantage against big companies able to hide profits all over the world, would be back on a level playing field.

Hickey pointed to Jia Lynn Yang writing at The Washington Post’s Wonkblog, Have U.S. states figured out a way to avoid a global race to the bottom on taxes? "... a number of states have come up with a simple way to calculate what firms owe them in taxes: If a company sells its product or services in a given state, it pays a tax proportionate to the sales in that state."

Harold Meyerson echoed this the other day in his column at the Washington Post, Apple’s U.S. revenue should be taxed,

There may, however, be another solution: taxing corporations on their revenue rather than their profits. If Apple gets 60 percent of its revenue from sales in the United States, Apple should pay U.S. taxes on that revenue. Let France collect taxes from Apple on its sales in France, China on its sales in China and so forth. Taking production and the location of corporate headquarters out of the equation would end the noxious practices of placing factories where the taxes are lowest and creating dummy subsidiaries to funnel profits through low-tax countries. Companies would still roam the globe in search of the cheapest labor, though a better Congress might one day seek to reward businesses for keeping and generating high-value-added jobs in the United States.

This idea comes from Bill Parks, who explained it in a recent USA Today op-ed, End abusive offshore tax loophole,

The good news is that California has developed a simple solution that neutralizes this loophole, Proposition 39. It works like this: A company that sells its products or services in California will pay income tax related to those sales.

For example:

- ABC Corporation has $10 million of sales of MP3 players in 2012.

- $1 million of those sales (10 percent of total sales) are made in California.

- ABC Corporation's total worldwide profit from all MP3 sales is $1 million.

- 10 percent of that profit is related to California sales.

- So 10 percent of ABC Corporation's worldwide profit will be taxed by California as California income.

Notice that it does not matter whether the ABC Corporation is a California, U.S., multinational or foreign corporation.

Tax them where they sell, instead of where they claim profits. It works for me.

P.S. Some argue that we shouldn't tax corporations because they just "pass through" taxes onto their customers through higher prices. But income taxes are on profits, and companies optimally price their products to maximize profits, which means they can't increase prices to cover taxes without reducing profits. And if they lowered profits, they would have lower taxes, and could lower the price and have higher profits, but then they would have to raise the price ... Or if they had mispriced their products before the taxes were calcuated and were charging too little, a price increase to cover taxes would mean even more profits which would mean they would owe more taxes, which would mean they would have to raise prices even more, which would mean ... eventually they would charge infinity. Only phone and cable companies can do that.

-----

Follow me and CAF on Twitter: